Sadly, the exhaustively quoted “Recovery Is a Marathon, Not a Sprint” has never been so true as it has been over the past few months. In July, the global box office scored $3.2 billion, the biggest result since the start of the Covid-19 pandemic. A significantly weaker release calendar in the following months had been slowing down the recovery. With a global total of $1.7 billion, November stabilized the status quo more than it was able to speed the recovery up again on a global scale.

Huge hopes were put on the long-awaited release of BLACK PANTHER: WAKANDA FOREVER. Expectations were too vast for one global blockbuster release after the multiple month-long voids to drastically elevate the recovery. However, it did perform very well. At the end of November, it already collected nearly $700 million worldwide, representing roughly 40% of the month’s global box office.

That currently puts it #7 in the 2022 ranking, just after THOR: LOVE AND THUNDER ($761 million) and THE BATMAN ($771 million), which it will overtake in the coming weeks. In the Domestic market, it’s already the #3 highest-grossing title of the year and #4 since the beginning of the decade. Its $381 million total put it a glimpse ahead of JURASSIC WORLD: DOMINION ($376m) at the beginning of December. Although still running strong, it’ll stay behind the first, record-breaking BLACK PANTHER’s global results being #14 of the global ($1.38bn) and #6 ($700m) of the domestic records.

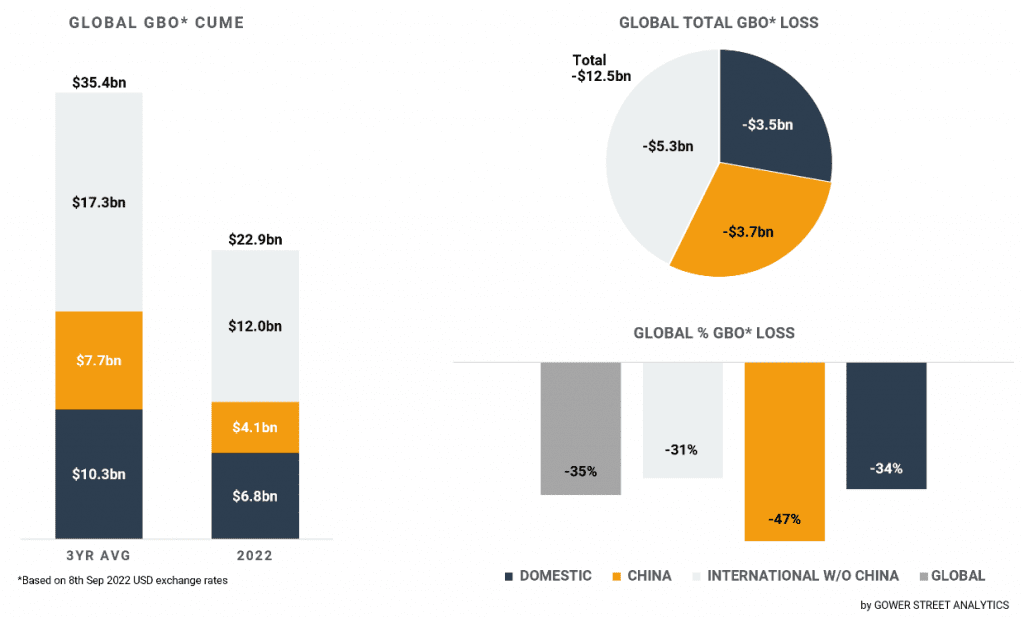

At the beginning of November, the global running year finally overtook the 2021 full-year result of $21.3 billion (historical exchange rates). It finished the month at $22.9 billion. While currently being 8% above the whole year of 2021 and 94% above 2020, it’s still tracking -35% below the average of the last three pre-pandemic years at the same point in time; a box office deficit of approximately $12.5 billion!

On this month’s GBOT (above), the stacked bar graph on the left shows total box office levels split out by the three key global markets: Domestic, China, and International (excluding China). The pie chart indicates the current deficit compared to the average of the past three pre-pandemic years (2017-2019) and where those losses are currently coming from. The bar graph on the bottom right displays the percentage drops globally.

The Domestic market contributed 38% of the global box office in November, with a monthly total of $628 million. That is its biggest share of the year to date, on par with the one achieved in June. It’s the 4th highest-grossing month of the year so far and the 6th highest since February 2020, upon the prior month by +29%. More importantly, it’s the first time in three months that the month is tracking ahead of the same month last year ($542m, +16%). Against the month’s average of the last three pre-pandemic years, it was, however, down -35%.

The aforementioned BLACK PANTHER: WAKANDA FOREVER naturally accumulated most of the domestic November box office with an impressive market share of 60%! It was the first title to gross more than $300 million within a month since July. Holdover titles BLACK ADAM, with $50 million (8%), and TICKET TO PARADISE, with $31 million (5%), also added reasonable amounts.

At the beginning of December, the Domestic market’s 2022 box office total stands at $6.8 billion. This is already 51% above the whole year of 2021 ($4.5bn) and 209% above 2020 ($2.2bn). Nevertheless – almost mirroring the global status – it’s still -34% below the average of the last three pre-pandemic years at the same time. A box office value of approximately $3.5 billion!

While the road to recovery is continuing to generally point upwards for the Domestic market, the opposite must be said about China. After being the first major market to reach significant levels of recovery, the market lost track in 2022. With just one month to go, China has a cume of $4.1 billion. That is $2.3 billion (-36%) behind the total at the same point last year! It’s further only slightly more than half of the box office that has been reached on average in the last three pre-pandemic years (-47%) in that period, around $3.7 billion less!

November marked another dramatic point in the Chinese downward spiral. With a monthly gross of $81 million, it’s the lowest grossing month since July 2020 ($31m), when cinemas just started to re-open after six months of closure. Only April this year ($82m) came in below the $100 million mark since. It’s just the 4th highest-grossing territory globally in November. This month China’s cinema industry suffered severely once again due to the country’s zero-covid strategy. The number of cinemas open by market share fell from a modest 66% at the beginning of the month to just 54% at the end. This is the lowest level since the week of April 16.

Around half of the month, the box office was delivered by two titles. Chinese local thriller THE TIPPING POINT contributed $20 million. Japanese anime release, DETECTIVE CONAN: THE BRIDE OF HALLOWEEN, added $17 million. That lifted the film’s lifetime global box office to $105 million. It was already the highest-grossing film in the long-running franchise in Japan ($77.2m) after being released there in April this year. It has played across the Asia Pacific as well as in key European markets, including Saudi Arabia, Germany, France, and Spain.

It was one of two Japanese movies this month that left a major mark outside its country of origin. Anime smash ONE PIECE FILM: RED added a further $25 million from new releases across multiple international markets. Over half of it was coming from the domestic market with $13.4 million. This pushed the cume outside of Japan up to $48 million! Illustrating once more the capability of Japanese movies to travel.

In its country of origin, the title added another $6 million in its 4th month of release to its now $137 million total there. But that wasn’t the main November story in Japan. It was the dominating local anime release of SUZUME’S DOOR-LOCKING with around $50 million box office, clearly refusing BLACK PANTHER: WAKANDA FOREVER, the #1 rank in the month, that it got nearly everywhere else.

SUZUME is the new movie by director Makoto Shinkai, whose prior two movies were also tremendously popular. WEATHERING WITH YOU is the 14th highest-grossing movie in Japan of all time. YOUR NAME is #5 and became the most successful Japanese film of all time at the global box office with over $358 million. SUZUME started to follow that path.

Regularly creating local phenomena like these helped Japan become the leading global market, referring to recovering from the pandemic. It has by far the smallest gap to pre-pandemic results of all major markets for the running year, currently being just -12% below the average of the last three pre-pandemic years! In November, it was +4% above the pre-pandemic average for the month.

Regionally, Asia Pacific (excluding China) is lifted by the performance of Japan. At the end of November, its cume for 2022 – as the single month itself – was down -27% against the three-year average. That is the least among the three sub-regions. Two more markets that also support the region’s strength are Australia, with -21%, and New Zealand, with -25% below the three-year average. The volatile performance of South Korea puts the market significantly below the sub-region average of -39%.

The highest-grossing sub-region, Europe, Middle East, and Africa (EMEA), is closer to the Domestic and global total levels at -33%. In November, it was -36% below the average box office for the month. The region is, of course, pulled down by Russia with its aggression-caused US studio boycott. It’s currently -56% behind.

Major markets like the Netherlands (-21%), France (-27%), UK/Ireland (-28%), and Germany (-29%) are performing better than the sub-region as a whole. At the same time, two major markets are sitting at the other end with Spain (-39%) and especially Italy, which is just having half of the box office accumulated for 2022 at the end of November as they had on average in the same period in the last three pre-pandemic years!

Latin America, the lowest grossing sub-region, is sitting between APAC and EMEA on the road to recovery: -31% down on the three-year average at the beginning of December. It was the best of the three in November at -26%. For the Latin American region, it was the 4th lowest number of the year so far, driven by the strong performance of BLACK PANTHER: WAKANDA FOREVER. The three major markets of the region Mexico (-32%), Brazil (-32%), and Argentina (-28%), are all performing in the same ballpark as the sub-region as a whole.

Whether the gap to pre-pandemic performances can be further reduced this year is mainly up to the sequel to the global highest-grossing movie of all time: AVATAR: THE WAY OF WATER. The first installment collected $2.9 billion over the last 13 years since its initial release. In December last year, SPIDER-MAN: NO WAY HOME was released, which showed the immense potential of the post-pandemic theatrical marketplace.

Ending at $1.9 billion and is currently #6 of the highest-grossing movies of all time globally. All chances are there to end the year on a high again. Nevertheless, with the risk of falsely putting the future of the business on a single movie again, a more consistent, diverse, and uninterrupted release calendar would be preferable to reduce the volatility of the theatrical market in the years to come.